A new projection from economists tracking women’s financial inclusion across the continent reveals a number so sobering it reframes the entire development conversation.

The number

At a ministerial dialogue held on the sidelines of the United Nations Economic Commission for Africa’s 2026 conference, an economist named Theophiline Bose-Duker presented a finding that should have made headlines around the world.

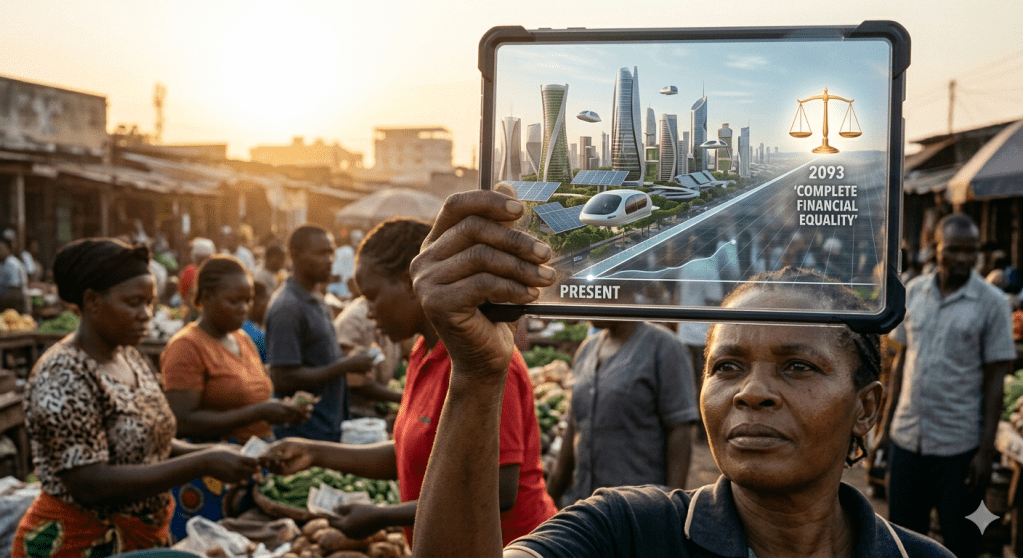

Africa’s average financial inclusion score, she said, has risen from 45.6 in 2011 to 53.5 in 2022. Progress, by any measure. But progress at what rate? At this pace, she told the room of finance ministers and development economists, full financial inclusion for women in Africa will not be achieved until 2093.

Sixty-seven years from now.

The room moved on to the next agenda item.

What the number contains

The 2093 figure comes from the African Centre for Economic Transformation’s African Women’s Inclusion Index, a composite measure that tracks women’s access to financial accounts, credit, insurance, pensions, and digital financial services across the continent.

The headline account-ownership numbers have improved significantly, largely driven by mobile money adoption. But the index tracks depth of inclusion, not just access, and on the deeper measures, progress has been close to flat. Women across Africa remain disproportionately excluded from formal credit (the product that builds businesses), insurance (the product that prevents catastrophe), and pensions (the product that prevents poverty in old age).

“Without gender-responsive data, we are effectively making policy with partial sight,” said Hannah Ryder, presenting findings from the ECA. “The less we measure, the more we undervalue both the cost of exclusion and the benefits of reform.”

Morocco’s finance minister, Nadia Alaoui, went further. Women’s exclusion from economic opportunity, she said, is rooted in governance failure, not in women’s capabilities or ambitions.

“Full financial inclusion for African women will not be achieved until 2093. That is a sobering reality.” — Theophiline Bose-Duker, ACET, UNECA 2026

What does 2093 mean on the ground?

In Nairobi’s informal settlements, the gap between mobile money access and genuine financial power is visible in every chama meeting, every market stall, and every woman who has a phone but cannot get a business loan.

Kenya is held up as Africa’s financial inclusion success story. Access to formal financial services has grown from 26% in 2006 to over 84% for women today. But access to a mobile account is not access to credit. And credit is how wealth is built.

According to a 2026 UN Women report on financial inclusion in East Africa, women across the region face what researchers call “shallow inclusion”; they have accounts but cannot access high-value products. Gender gaps remain stark in formal bank credit, debit card ownership, insurance coverage, and pension participation.

The women who feel this most acutely are not in the statistics. They are in markets and fields and sitting rooms, running savings groups and informal credit circles because the formal system has repeatedly failed to design products for their lives.

What would actually change the timeline?

Economists and gender finance specialists consulted for this piece broadly agree on what accelerated progress would require. None of it is technically complicated.

First, sex-disaggregated data collection must become mandatory for financial institutions. You cannot close a gap you refuse to measure. Second, informal savings history, the years of contributions that millions of African women have made to chamas and ROSCAs, must be recognized as credit collateral. A woman who has saved consistently for a decade has a credit history. Banks simply will not read it.

Third, governments must stop treating menstrual health, unpaid care, and informal labor as separate issues from financial inclusion. They are the same issue. The time women spend on unpaid care is time they cannot spend earning. The income they lose to period poverty and inadequate health protection is income they cannot save or invest.

“Closing the gender gap could boost Africa’s GDP significantly,” said the World Economic Forum in a 2025 report. “But we keep treating it as a social issue rather than an economic one.”

The question behind the question

The 2093 projection is not a natural disaster. It is a policy choice. Every year that passes without gender-disaggregated data requirements, without chama savings recognized as collateral, and without menstrual health funded as a labor issue adds another fraction to that timeline.

The finance ministers who heard Bose-Duker’s number at the UNECA conference in 2026 applauded. They signed a communique acknowledging the need for accelerated action. Then they flew home.

In Nairobi, Grace Muthoni was already at the market for her 3 a.m. shift. In Mathare, Margaret Wanjiru’s chama envelope was on the table. In Eastleigh, women were counting fabric bolts and tallying loans.

They are not waiting for 2093. They never were.

The question is whether the people with the power to change the timeline will start treating it as a crisis before the decade is out.

Data sources: African Centre for Economic Transformation, African Women’s Inclusion Index 2025; UN Women East Africa Financial Inclusion Report, February 2026; UNECA Ministerial Dialogue on Women’s Financial Inclusion, 2026; World Economic Forum Gender Gap Report, 2025.

Leave a comment