africa-creators-digital-economy-monetization-gap

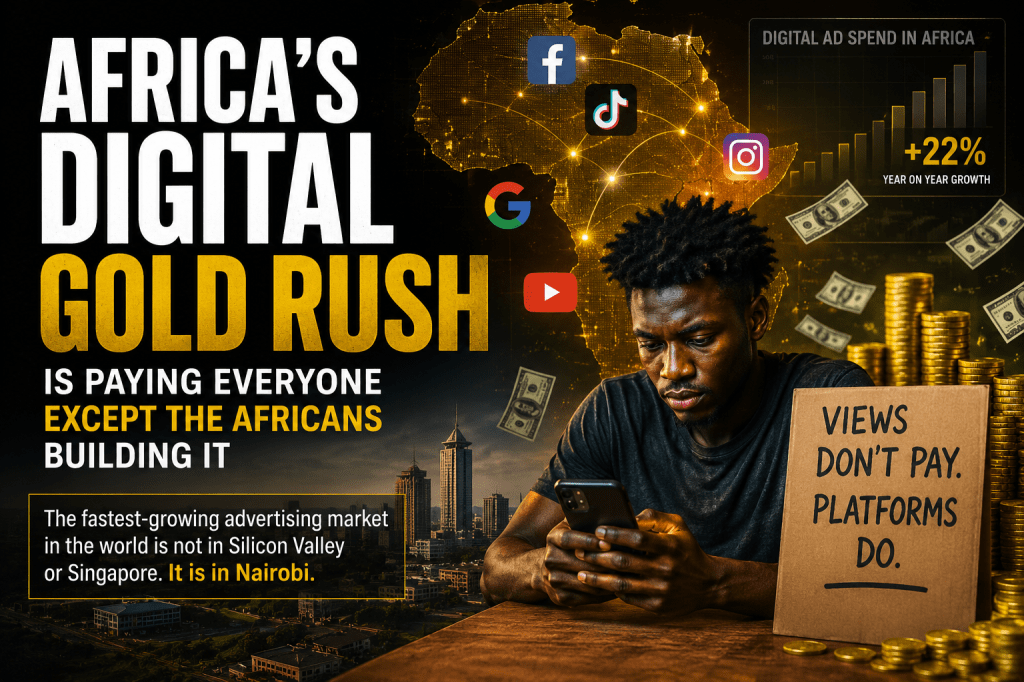

The fastest-growing advertising market in the world is not in Silicon Valley or Singapore. It is in Nairobi.

PwC’s Africa Entertainment and Media Outlook 2025-2029, published in October 2025, ranked Kenya as the world’s fastest-growing internet advertising market, projecting a 16 percent compound annual growth rate through 2029, faster than any country on the planet. Nigeria posted 11.2 percent entertainment and media growth in 2024. Africa’s creator economy, now valued at $3.08 billion, is on track to reach $17.84 billion by 2030, according to the African Creator Economy Report 2.0 compiled by Communique and TM Global. The numbers read like a press release from a continent that has finally, definitively, arrived.

The creators generating that growth are earning less than $100 a month.

I have walked past the Sameer Business Park in Westlands more times than I can count. Roadside vendors working the pavement outside. Minibuses turning north toward Parklands. The complex itself looks like any other corporate cluster in Nairobi, glass and concrete and a security barrier, nothing outside announcing what happens in the floors above. For years, workers employed by Sama, a San Francisco-based outsourcing firm contracted to Meta and OpenAI, sat in that building and annotated content, eight consecutive hours at a screen, deciding what was real and what was dangerous and what the AI systems of the world’s most valuable companies should learn to see. They were paid, according to documents obtained by Time magazine, around $2 an hour. OpenAI had agreed to pay Sama $12.50 per hour per worker. The distance between those two figures is where much of Africa’s tech story lives.

The argument I hear most often about Africa’s relationship with global technology is that the continent is catching up. What the data shows is something else entirely. Africa is not catching up to anything. African creators, African workers, and African audiences are generating real economic value right now, in 2026, and the architecture of that value, who builds it, who captures it, who profits from it, is designed almost entirely in other people’s interests.

The numbers and who gets them

The African creator economy sits at $3.08 billion, according to the African Creator Economy Report 2.0, heading toward $17.84 billion by 2030 at a 28.5 percent annual growth rate. Across YouTube, TikTok, and Instagram, 272.4 million advertiser-targetable accounts exist in Nigeria, Kenya, Egypt, and South Africa alone. Advertising markets in Lagos and Nairobi are outpacing London and Toronto in growth rate. By 2029, digital advertising will account for 64 percent of Kenya’s total ad spend, PwC projects, with video advertising climbing at a 22.3 percent annual pace.

Yet roughly six in ten creators across the continent earn less than $100 a month from their work, per the same report, released in February 2026. Platform advertising revenue, the direct payout from views on YouTube, TikTok, and Meta properties, accounts for just 5.8 percent of African creator income. Brand sponsorships carry 28 percent. Digital product sales, 25 percent. The mechanism of growth and the mechanism of payment are running on entirely separate tracks.

This is not coincidence. It is policy.

Locked out by design

TikTok’s Creator Fund covers the United States, the United Kingdom, Germany, France, Brazil, Japan, and South Korea. Zero African countries are eligible, as OkayAfrica reported in January 2025. The Creator Rewards Programme, TikTok’s replacement scheme, covers 53 global regions. Only Morocco, Egypt, and South Africa make the list. Kenya does not. Nigeria does not. Ethiopia, Ghana, Tanzania, Uganda, Senegal, Cote d’Ivoire, none of them qualify.

This is not a minor technical limitation. In Nigeria alone, TikTok counts 6.3 million creators with at least 1,000 followers, according to data compiled by Contemeleon in January 2026. Every view those creators generate earns ad revenue for TikTok. None of it flows back to the creator. It flows to ByteDance.

Think about that. Millions of people producing content, building audiences, training the recommendation engine, and receiving nothing for the views their work generates. Not a small percentage. Nothing.

David Adeleke, founder and CEO of Communique, the Lagos-based media and intelligence firm that produced the African Creator Economy Report, has described the gap without softening it. He told CNBC Africa that the next phase of Africa’s creator economy depends on the emergence of more local platforms, because the global ones were not built to share value with African audiences. The star alignment he described, market readiness, audience demand, distribution technology, is real. What remains misaligned is where the money lands.

Only 4.2 percent of African creators have secured any formal institutional investment, per the African Creator Economy Report 2.0. Ninety-five percent operate outside institutional finance entirely. The sector has 385 million active social media users and a growth rate that outpaces global benchmarks by multiples. It has almost no access to the capital structures that would let creators own a meaningful share of what they build.

The hidden labor floor

The monetization gap for creators sits on top of something older and uglier. The AI systems those same platforms use to rank content, moderate posts, and personalize feeds are built, in part, on labor routed through Nairobi.

An investigation published in March 2026 by Swedish newspapers Svenska Dagbladet and Goteborgs-Posten, later followed by reporting from The Next Web, Rest of World, and other outlets, revealed that workers employed by Sama in Kenya had been reviewing footage from Meta’s Ray-Ban smart glasses, including intimate images filmed without the subjects’ knowledge. Workers told the Swedish publications they had seen footage of people using the toilet and engaging in sexual activity. Less than two months after those accounts were published, Meta terminated its contract with Sama. On April 16, 2026, 1,108 workers received formal redundancy notices.

Naftali Wambalo, co-founder of the Africa Tech Workers Movement, alleged the termination was retaliation against workers who had spoken out. Meta has not responded to that allegation. The Kenya Office of the Data Protection Commissioner opened an investigation. The UK Information Commissioner’s Office wrote to Meta calling the reports “concerning.” A class action lawsuit is pending.

A pattern visible across the AI labor supply chain in Kenya for years: technical documents and prior reporting show the same structure repeating. OpenAI agreed to pay Sama $12.50 per worker per hour. The workers received approximately $2. Sama said that was a fair wage for the region. The workers, many of whom developed symptoms consistent with post-traumatic stress from sustained exposure to violent and disturbing content, disagreed. Kenya markets itself as East Africa’s tech hub, home to what its government calls Silicon Savannah. For thousands of Nairobi’s workers, the jobs that label describes involve annotating traumatic content in a building off Waiyaki Way for a fraction of the wages the Silicon Valley client agreed to pay.

The people who train the AI see everything. Then they lose their jobs when they say so.

What the market already knows

The potential is not in doubt. PwC is not an optimistic think tank. When a firm that size ranks Nairobi as the world’s fastest-growing internet advertising market, that figure has been stress-tested. When projections show Africa’s creator economy growing at 28.5 percent annually against a global creator economy Goldman Sachs pegged at $240 billion in 2024 and heading toward $530 billion by 2027, those are not aspirational numbers. They are current market realities already priced into ad rate projections and platform expansion strategies.

Local platforms are building the alternative. Selar, the Lagos-based creator commerce platform, paid out 9.8 billion naira to African creators in 2024, roughly $6 million, showing that direct-to-audience models work at scale in African markets when they are built for those markets. Mdundo, the music distribution platform operating across East and West Africa, reached 39 million active users in 2025 and paid $1 million in royalties to more than 300,000 artists between January and July of that year. These are not workarounds. They are the first beams of a different architecture.

But local platforms at those scales cannot yet absorb the value that global platforms are extracting. The gap, between what African creators generate and what they receive, between what AI companies earn from African labor and what those workers are paid, is not a natural market outcome. It is the result of choices embedded in product roadmaps, monetization eligibility lists, and outsourcing contracts. Choices, which means they can be changed.

One reason this matters to a reader anywhere

The argument that this is an African problem, contained to a continent, does not survive examination. The AI systems trained in Nairobi operate globally. The content moderation decisions made by Kenyan workers shape what appears on platforms used by two billion people. The creator economy models being stress-tested against Africa’s mobile-first, high-growth markets are the models global platforms will deploy everywhere next. Africa, as it has been in mobile money, in direct-to-consumer finance, in short-form content consumption, is the proving ground for what digital economies look like when infrastructure is constrained and audiences are young, numerous, and building something with their own hands.

The question is whether the people building it will be allowed to own any of it this time.

I live in the city that is apparently home to the world’s fastest-growing internet advertising market. I also live in the city where 1,108 workers who trained the AI behind that growth were handed redundancy notices in April, after they told the truth about what they had seen. Both of those things are true at the same time. That is the story most international coverage of African tech keeps missing, the extraordinary growth and the extraordinary extraction, running side by side, in the same city, sometimes in the same building.

The gold rush is real. The people doing the digging need to decide who owns the mine.

Leave a comment